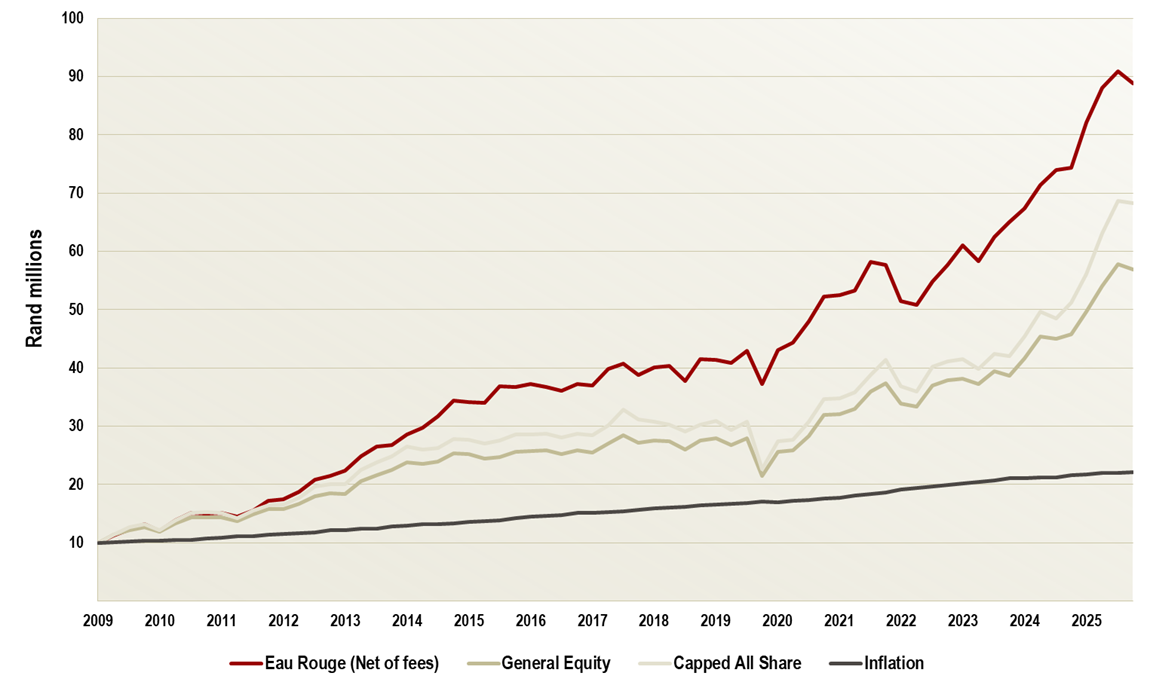

Our powerful performance track record reflects that we are achieving our mandate of improving the well-being of our clients over the longer term. Our local performance, in particular, has been a source of consistent returns. We have meaningfully outperformed the General Equity Unit Trust and the Capped SWIX over the life of the business, having compounded the value of portfolios at 13.9% per annum for nearly 17 years.

Illustrative performance data to 31 March 2026

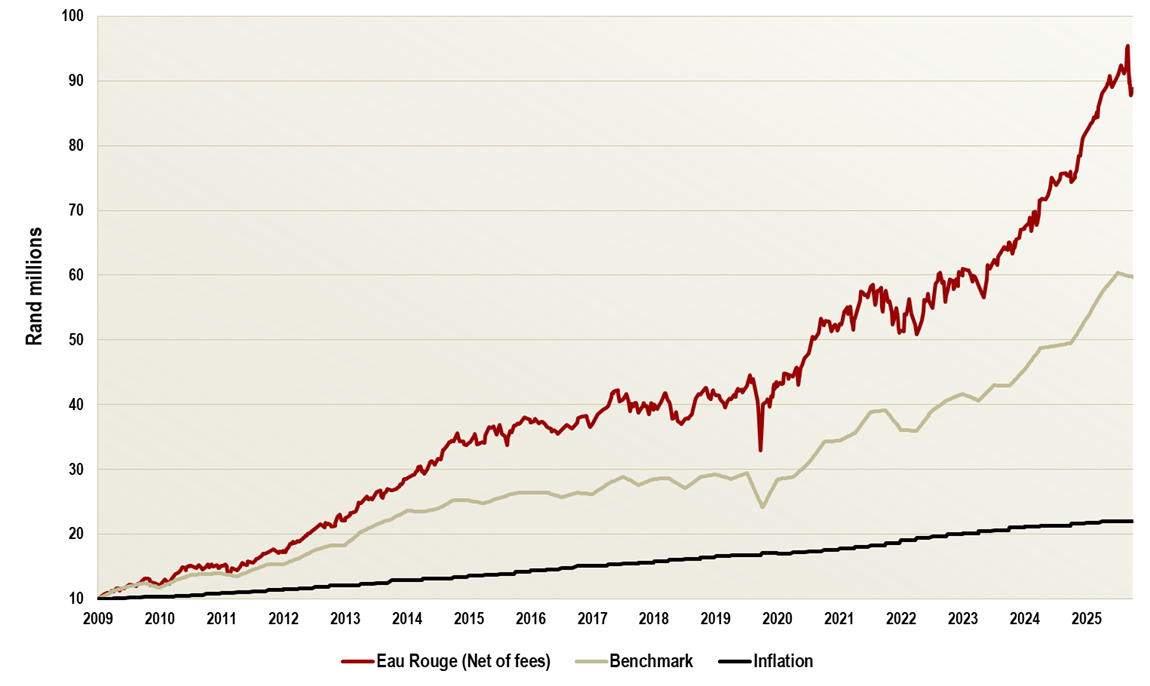

Set out below is the performance, since inception, of the Eau Rouge model portfolio against our composite benchmark. We have established a proud history of outperformance over longer-term periods, both locally and offshore. We remain among the very best in class compared to the universe of domestic general equity unit trusts in South Africa, through both bull and bear markets. This reflects our disciplined investment process and balanced investment philosophy.

Our composite benchmark is comprised of 80% South African General Equity unit trusts and 20% offshore (60% MSCI All Country World Equity, 30% Bloomberg Global Bond, 10% JPMorgan cash index).

A very comprehensive and detailed performance analysis is prepared quarterly, covering both local and offshore attributions. Due to the intricate detail inherent in the management of segregated account mandates and the related measurement of performance, this information is not made available on this website, but is included within the Eau Rouge brochure for presentation to prospective clients at our initial meeting.

The performance reflected above is that of the Eau Rouge model portfolio and is provided for illustrative purposes only. We are highly disciplined in applying investment decisions uniformly across segregated portfolios to ensure coherence and consistency, yet pragmatic in order to accommodate specific client needs and diverse tax regimes. Eau Rouge utilizes sophisticated custom-made tools and techniques to monitor portfolios on a daily basis, which enables us to achieve high levels of consistency between individual portfolios and the model. This process ensures that the performance of the hypothetical model portfolio closely resembles an actual portfolio of R10 million invested at 30 June 2009. Nevertheless, actual portfolio performances tend to differ from the model to some extent depending on, for example, typically small variations in portfolio weightings, individual client income and capital requirements and varying brokerage rates according to transaction sizes. The model portfolio reflects all the investment decisions taken by Eau Rouge at the respective dates. Dividend and interest income is assumed to be reinvested when paid and the performance of the model portfolio is calculated after applying the standard scale of brokerage fees and marketable securities tax. Cash returns reflect the actual interest rate paid by the JSE Trustees and is stated before tax. Management fees are excluded in order to present valid comparisons with the appropriate market indices. A schedule of the Eau Rouge fee structure is available here.

The general equity return shown above reflects the median return of Morningstar’s domestic general equity unit trust universe. This comprised of 104 funds with a combined value of R305 billion at 31 March 2026. As regards the performance of the general equity unit trusts, it is important to note that unit trust prices measured on a net asset value basis reflect management fees and fund expenses, but do not take any upfront managers’ fees into account.

Existing and prospective clients are reminded that the value of their investments and any income that they may derive therefrom could rise or fall, and therefore they may not fully recover the amount invested. In other words, investment returns and principal value fluctuate, so some or all of the investments in portfolios managed by Eau Rouge may be worth more or less than the original cost and current performance may be higher or lower than that presented herein. Past performance is not a reliable indicator of future results and prospective investors should take care to ensure that their investment horizon is over the longer term. Investors should also consider the risks related to currency movements on various investments that may be included in Eau Rouge’s investment portfolios from time to time, which may include the risk of lower investment returns and/or loss of value. The returns on the associated segregated portfolios managed by Eau Rouge from time to time are never guaranteed.

The following statements are intended to summarise some of the risks, but are by no means exhaustive, nor do they offer advice on the suitability of various investments.

There is no guarantee that the investment objectives of Eau Rouge’s investment process or of any of our clients will necessarily be achieved.

Past performance is not necessarily indicative of future performance. Assets perform differently over varying time periods and these differences tend to be magnified if investments are measured over shorter time periods. This renders very short term comparisons almost meaningless but, equally, very long term comparisons suffer deficiencies as well, given the extensive changes which tend to occur in economic, monetary and other background fundamentals over the longer term. In South Africa, for example, the structural decline in inflation which began in 1993 resulted in the subsequent prolonged outperformance of bonds relative to equities until 2004.

Nevertheless, investments in securities generally perform better and are associated with lower risk when structured as medium to long term investments. The Eau Rouge investment process is predicated on an extended investment horizon.

Investment returns are also dependent on the performance of the underlying asset classes to which clients’ portfolios are exposed from time to time, both locally and internationally. To this end, a research note is enclosed in Eau Rouge’s brochure and presented to prospective clients after our first exploratory meeting with them. The purpose of the comparative study of returns of different asset classes in South Africa, and internationally is:

The research report also illustrates the effect of tax on various asset class returns.

Some of our clients’ offshore funds may be invested in emerging markets from time to time. The legal, judicial and regulatory infrastructure is still developing in these regions and there may therefore be some legal uncertainty both for local market participants and their overseas counterparts. Some of these markets may carry significant political, economic, accounting practices, shareholder, market and settlement, currency, taxation, execution and other legal risks for current and prospective clients of Eau Rouge, who should therefore ensure that they understand the relevant risks and opportunities that these markets may present from time to time and satisfy themselves of the suitability of these investments before signing an investment mandate with Eau Rouge.

Clients’ funds may be invested in a number of investments denominated in a number of different currencies outside of the rand monetary area. Accordingly, changes in foreign currency exchange rates may adversely affect the value of these investments and any income derived therefrom.

Interest rate fluctuations affect the capital value of these investments. Where long term interest rates rise capital values are likely to fall, and vice versa. The value of a bond will also fall in the event of the default or reduced credit rating of the issuer (or if credit spreads widen relative to government bonds), similarly an increase in credit rating (or narrowing of credit spreads) can lead to capital appreciation. Generally, the higher the rate of interest on any bond, the higher the perceived credit risk of the issuer. However, the impact of any default is reduced by diversifying the portfolio across a wide range of issuers and regions. The yield (and hence the market value) will also depend on the market environment and economic conditions.

We are very hands-on in diligently managing our clients’ investments, fine-tuning a wide array of complex aspects to ensure investments are protected whilst driving hard to maximise return.

- ALBERT EINSTEIN

We strive to be conscientious stewards of the capital our clients have entrusted us to manage....

We are one of the very top performing investment houses in Southern Africa....

Sustaining cutting edge performance demands continual research and development, and investment in ....

The security of your investments is of the utmost importance to us. You retain direct and immediate....

We are one of the very top performing investment houses in Southern Africa, with our longer-term performance comparing favourably with best-of-breed asset managers.